Income feels more stable when you know what is yours to spend, what belongs to future obligations, and how different income streams fit together. Without that visibility, even strong earnings can feel unreliable.

1. Why Income Tracking Matters

Many people track spending but treat income as obvious. That is a mistake when income is variable, mixed across sources, or partly reserved for tax and other future obligations.

2. Gross Income Is Not Fully Usable Income

What lands in your account is not always what you can safely spend. Freelance income, consulting revenue, bonus payments, and business-related earnings often require a reserve mindset rather than a consumption mindset.

When you separate earned income from usable income, financial decisions become much calmer.

3. How to Reserve for Tax Simply

You do not need a complicated tax model to start planning responsibly. What matters is that part of qualifying income gets reserved consistently instead of being mentally counted twice.

- Track income by source.

- Decide which sources need a tax reserve.

- Set aside a consistent percentage or fixed reserve based on your situation.

- Review periodically rather than waiting for pressure to build.

4. Handling Mixed Income Sources

If you have salary plus freelance or side income, avoid treating them identically. Stable salary may support your baseline budget, while variable earnings can fund taxes, buffers, goals, or debt acceleration.

5. A Review Rhythm That Keeps Things Calm

Review income weekly if it is variable and monthly if it is mostly stable. The aim is not constant anxiety. The aim is clear awareness before obligations catch up.

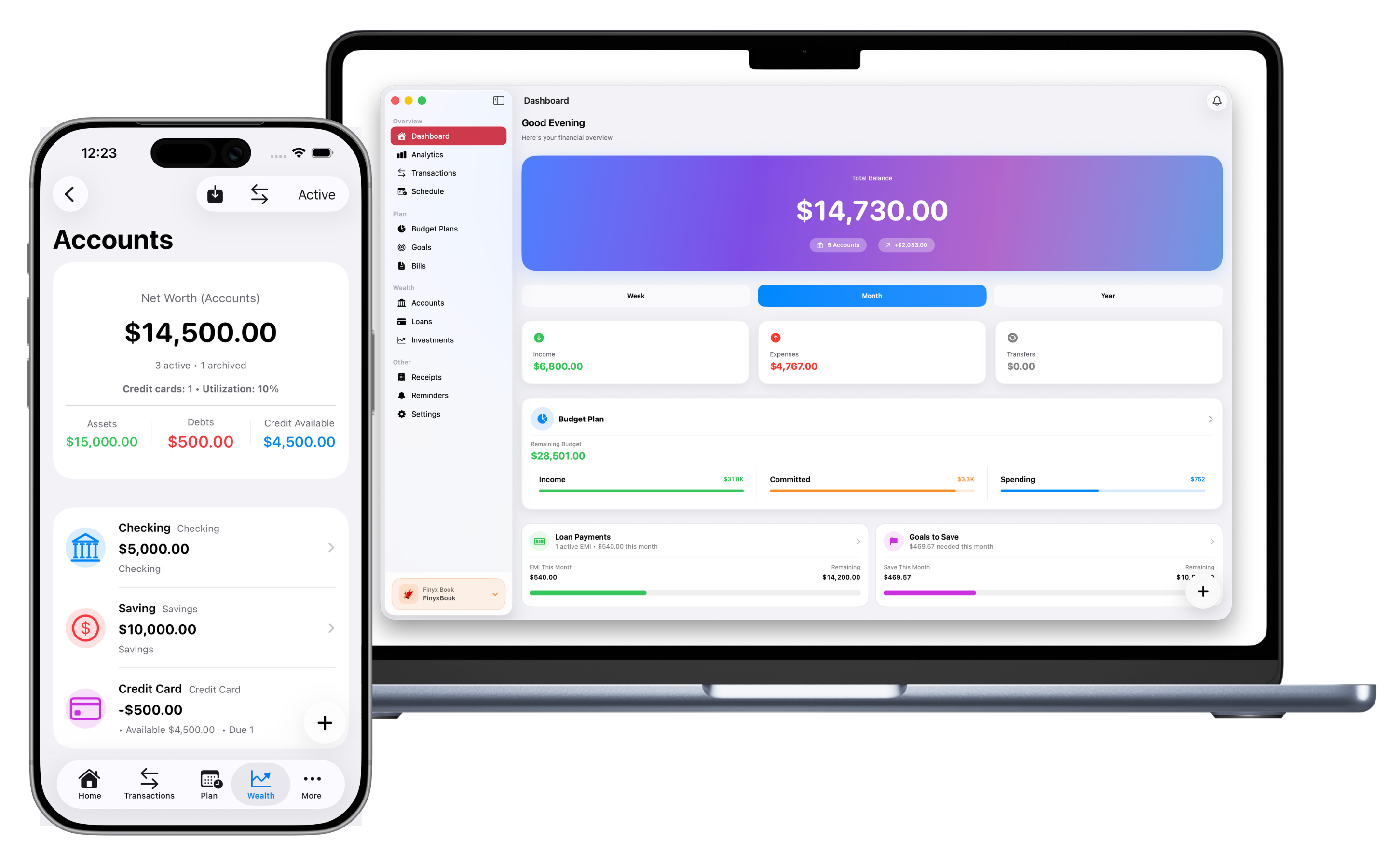

6. What to Do in FinyxFin

- Track salary, freelance earnings, side income, and transfers clearly.

- Use books to separate personal, freelance, or project income streams if that helps your workflow.

- Create goals for tax reserves or future obligations so that money is not mentally overcommitted.

- Review income alongside budgets, goals, and spending in one system.

Final Thoughts

Income tracking becomes much less overwhelming when you stop treating all incoming money as equally available. Clear separation creates better spending decisions and fewer future surprises.

When you know what income is for, the rest of your financial planning gets easier.