Most people do not fail with money because they lack information. They fail because they do not have a system that fits real life. When finances are scattered across notes, spreadsheets, bank apps, reminders, and memory, even smart people lose track.

Good money habits reduce friction. They help you make better decisions before money becomes stressful. The seven habits below are practical, sustainable, and designed for normal life — not idealized finance plans that only work on paper.

1. Build a Small Emergency Buffer

The first goal is not optimization. It is stability. A small emergency buffer changes how you experience unexpected expenses. Without savings, a broken appliance, medical visit, or repair often turns into new debt. With even a modest buffer, the same problem becomes manageable.

This is why emergency savings matter so much early on. They do not solve everything, but they stop short-term problems from becoming long-term setbacks. People often wait until they feel “ahead” before saving. In practice, saving first is what helps them get ahead.

If your bike breaks down and repairs cost $600, having cash set aside makes it an inconvenience. Without savings, it can become a credit card balance that stays with you for months.

Small emergency savings reduce financial stress because they give you time, options, and breathing room when something goes wrong.

- Create a dedicated goal called “Emergency Fund.”

- Set a target amount that feels realistic instead of waiting for a perfect number.

- Record each contribution so progress stays visible and motivating.

2. Track Expenses Consistently

Most overspending is not deliberate. It is invisible. Small purchases blend into the background, subscriptions become automatic, and irregular expenses slip through because they are not painful in the moment. Tracking changes that. It creates visibility, and visibility changes behavior.

The goal is not to obsess over every cent. The goal is to know where your money is actually going. Once you have that picture, you can make better decisions without guessing.

$25 spent here and $18 spent there may not feel meaningful on their own, but repeated daily or weekly, those habits quietly become hundreds of dollars every month.

- Add expenses as they happen so spending stays current instead of becoming a weekly catch-up task.

- Use categories consistently to reveal where money is going over time.

- Scan receipts when you want to reduce manual entry and turn real-world purchases into usable records faster.

3. Keep Budgeting Simple

The best budget is the one you can keep up with. Complex budgeting systems often fail because they demand too much effort. A simple budget is not less serious. It is more sustainable.

Most people do better when they start broad: essentials, flexible spending, and savings. Once the habit is stable, detail can be added later if it is genuinely useful.

Budgets fail when they become a bookkeeping project. They work when they help you make decisions quickly.

- Create a few practical budgets you can realistically maintain.

- Review how much is left instead of trying to memorize your limits.

- Use the structure to guide choices during the month rather than only reviewing after the money is gone.

4. Reduce High-Interest Debt First

High-interest debt is expensive not only financially but mentally. It narrows your options, delays savings, and makes progress feel fragile. If you are paying high interest, your money is working against you before it has a chance to work for you.

The exact payoff strategy can vary, but the core principle is simple: make debt visible, give it a plan, and stop letting it run in the background.

A $5,000 balance at high interest can stay around far longer than expected if you are only making minimum payments and not tracking the bigger picture.

- Add each loan so balances and repayments stay visible.

- Track progress over time instead of treating debt as an invisible monthly drag.

- Keep debt in the same system as your spending and savings so trade-offs are easier to understand.

5. Start Investing Early

Investing is less about finding the perfect moment and more about building the habit of consistency. Many people postpone investing because they feel they do not know enough, do not have enough, or should wait until the rest of life feels more organized. That wait can last years.

Starting small matters more than starting perfectly. When investing becomes part of your routine, it stops feeling like a special event and starts becoming normal behavior.

Someone who invests $200 every month for years is often in a stronger position than someone who keeps waiting for the “right time” to begin.

- Add your investment accounts and holdings in one place.

- Track contributions so progress feels connected to your broader financial life.

- See investing alongside goals, budgets, and expenses instead of managing it in isolation.

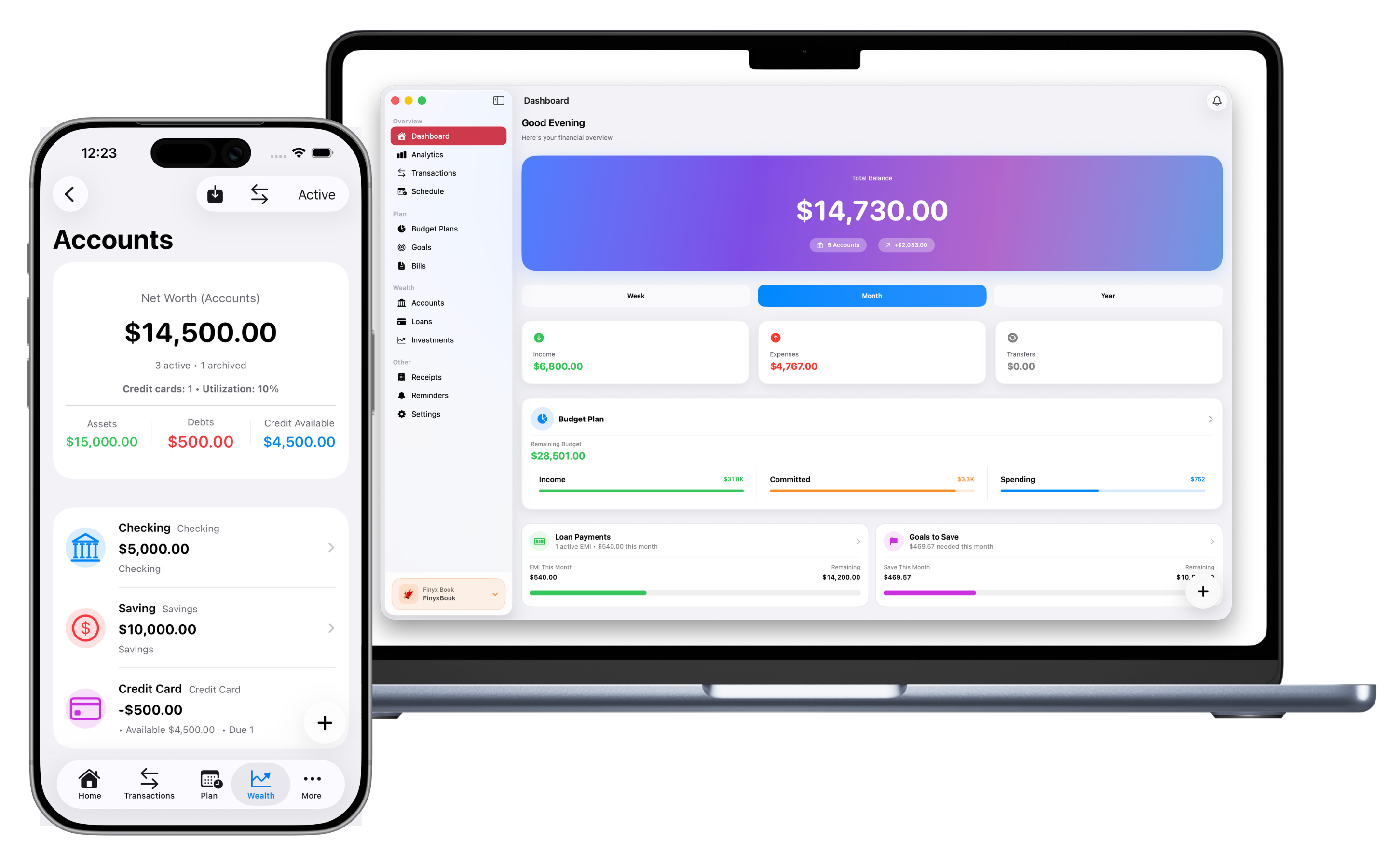

6. Organize Your Finances in One System

A surprising amount of money stress comes from fragmentation. Bills live in email. Expenses are half-tracked. Loans sit in one place, investments in another, and goals exist only mentally. Even when the numbers are manageable, the experience feels messy.

Organization is not about having more data. It is about having enough structure that the right information is available when you need it.

When everything is visible in one place, decisions become faster, calmer, and less reactive.

- Keep expenses, budgets, bills, goals, loans, and investments in one app.

- Use multiple books when you want to separate different parts of your financial life.

- Track across multiple currencies when your finances span more than one region.

7. Set Clear Financial Goals

Money becomes easier to manage when it is attached to something specific. Without goals, saving feels abstract and spending tends to win because it delivers immediate satisfaction. Goals create direction, and direction makes trade-offs easier.

A goal does not have to be dramatic. It can be an emergency fund, travel, a large purchase, or simply getting a certain account to a healthier number. What matters is that it gives your money a job.

Saving feels far more natural when it is tied to a named goal than when it is just “whatever is left over this month.”

- Create a goal for each major priority instead of keeping it in your head.

- Track progress visually so motivation does not depend on memory.

- Connect day-to-day saving with something meaningful and visible.

Final Thoughts

Financial control is rarely about discovering a secret strategy. More often, it comes from following a handful of good habits long enough for them to become normal.

The real value of a finance app is not adding complexity. It is reducing friction so the right habits are easier to maintain. That is where FinyxFin fits in: not as a replacement for good decisions, but as a practical system that helps you follow through on them.

Start small. Build gradually. Stay consistent.